Perfecting an advance pricing agreement application in China

China’s State Administration of Taxation (SAT) has released new rules for advance pricing arrangements (APAs), signaling that the authority is willing to work more closely with multinational companies (MNCs), align with global audit standards and construct a more advanced framework to plug tax loopholes.

On October 11, 2016, the SAT released the Announcement on Matters Relevant to Improving the Administration of Advance Pricing Arrangements (Announcement), replacing the APA rules under Chapter 6 of Guoshuifa [2009] No.2 (Circular 2). The new Announcement, which came into effect on December 1, revamped the APA application procedure and requirements. Soon after, on December 23, the SAT issued the 2015 China Advance Pricing Arrangement Annual Report (2015 Report), which summarizes China’s APA practice throughout 2015 and reaffirms the tax authority’s expectations of improving the quality and efficiency of APA applications.

China has been running APA programs since the late 1990s. The first unilateral and bilateral APAs in China were signed in 1995 and 2005, respectively. The 2015 Report showed that from 2005 to 2015, despite a great increase in the total number of APA applications, the number of concluded APAs remained relatively small—in contrast to the size of China’s economy and foreign investment. These numbers illustrate a significant gap between the taxpayers’ enthusiasm to seek for tax certainty through APA applications and the PRC tax authority’s limited capacity in processing APAs to completion. Many MNCs have voiced frustration with the lack of resources in China’s APA program, and the latest Announcement seeks to address these concerns.

That said, increasing the number of successful APA cases is not the purpose of the SAT. As emphasized in the 2015 Report, the SAT has focused its efforts on boosting work efficiency and application submission quality, and will continue to do so. The detailed measures for these efforts are provided under the Announcement and will significantly change the dynamic in future APA applications in China. MNCs wishing to attempt APA applications in China must understand and take into consideration the fine details of the Announcement for opportunities and risk analysis.

The 2015 APA Annual Report

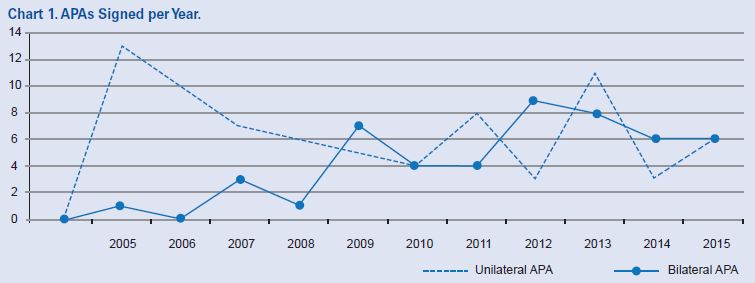

According to the 2015 Report, the SAT concluded 125 (76 unilateral and 49 bilateral) APAs in total from 2005 to 2015, averaging a signing of 10 to 13 unilateral and bilateral APAs each year. Chart 1 displays a very limited increase in the number of APAs concluded each year over the decade. The SAT has been providing extensive transfer pricing (TP) and APA training to tax officials at the provincial and local levels, and set up a third anti-avoidance division in 2015. These measures will help to increase the number of APA applications processed by the SAT in future, but the gap is not expected to be entirely bridged any time soon.

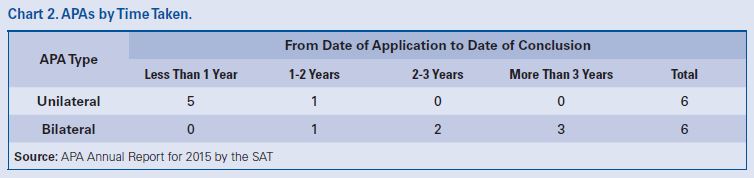

The report also reveals that a unilateral APA usually takes two years to complete, while a bilateral agreement can span more than three years. It should be noted this time period refers to the date of formal application to the date of conclusion—taking into account preparation and communication with the local tax authorities prior to submission means that the actual time cost for applicants is much more substantial.

The report indicates that 67% of the successful APAs were highly concentrated in the manufacturing sector and tangible products business. Only around 15% of the successful cases were in intangible transfer and use rights licensing, 18% in services, and none in the financing sector. Also, due to insufficient public data and in-depth TP analyses, the Transactional Net Margin Method (TNMM) was most commonly used, having been applied in 78.4% of the successful cases.

The SAT also stated that priority will be given to the following APA applications:

- cases where the applicants provide high-quality information and application documents;

- cases on inter-company services, intangible transfer and licensing, and financing; and

- cases where the Resale Minus Method, Profit Split Method or other non-TNMM method is used.

The new APA rules

Raised threshold

The Announcement requires a qualified APA applicant to have an annual inter-company transaction value of over Rmb40 million for each of the last three years prior to its submission of letter of intent. This is a more stringent requirement than the previous Circular 2, which only required a general annual amount of Rmb40 million.

Going forward, newly-formed enterprises will no longer be able to apply for an APA before establishing a track record that meets the three-year threshold. This may reduce the number of unilateral APA applications, but presumably will not have an impact on the number of bilateral APA applications, as most applicants of the latter are MNCs with sizable operations in China and large annual inter-company transaction values.

Application process

Under the Announcement, the APA application procedure is adjusted to include the following six steps:

Step 1 Pre-filing meeting between the applicant and the China local tax authority;

Step 2 The applicant’s submission of the letter of intent and APA proposal;

Step 3 The PRC tax authority’s analysis and evaluation of the APA proposal;

Step 4 The applicant’s formal APA application;

Step 5 Consultation and negotiation between the applicant and the PRC tax authority (and between the PRC and relevant jurisdiction’s tax authorities in the case of a bilateral APA); and

Step 6 Execution of the APA.

The key changes in this new procedure are:

- the inclusion of Step 2, where the applicants are required to prepare and provide very detailed and complete information on their inter-company transactions and the proposed APA arrangement; and

- the change of Step 3’s evaluation from after to before the formal application in Step 4, which allows the tax authority to conduct and complete the review and assessment work before officially accepting the APA applications.

These updates represent enhanced requirements for information disclosure and document submission, and will increase the burden of applicants before the official submission. There is a greater possibility for the process to be stopped before the formal application if the applicant fails to submit a high-quality analysis in the proposal stage.

In Step 3, the Announcement allows the tax authority to have on-site interviews and discussions with the applicant. The authority may also suggest changes to the submitted proposal. By the end of this stage, the tax authority and the applicant would have reached a certain consensus on the key contents of the proposed APA, which enables the following formal application and negotiation steps to be completed fairly quickly.

Given these changes, managing the information disclosure requirements in a bilateral APA application could be challenging for applicants. In many other countries, the full disclosure of inter-company transaction data and submission of a detailed proposal are only required after the tax authority’s acceptance of the formal application. Submitting to one tax authority before the official application and to the other afterwards would require greater coordination.

Greater disclosure and analysis

In comparison with Circular 2, the new Announcement has more disclosure and in-depth analysis requirements, including:

- value chain or supply chain descriptions;

- evaluation of cost saving, market premium and other location-specific advantages; and

- business operations and inter-company transactions of the relevant foreign related parties in the past three to five years (in the case of bilateral APA application).

The latest developments in Base Erosion and Profit Shifting (BEPS) actions in China require a complete value chain or supply chain description to be included in the local TP documentation for the year 2016 onwards. In an APA application, the required description remains consistent with the China TP documentation, but should presumably include more details and deeper analysis.

Most MNCs may have yet to analyze and factor in cost saving, market premium and other location-specific advantages in their TP arrangement for China. Explaining and justifying why such special advantages have not been taken into consideration before the APA application may be a challenge. It could also be very difficult to agree with the China tax authorities on the identification and assessment of location-specific advantages, given that there are still no specific rules under the China TP framework. Interpretation by the local authorities could be significantly different from that of others under the BEPS Action Plan.

Disclosing foreign related party inter-company transactions from the past three to five years could be an onerous burden, especially if there are multiple foreign related parties, different types of inter-company transactions, and changes in business operations. Adding to the complexity is if there are discrepancies between the expected and the actual inter-company transaction results of these foreign related parties, or if any of the related parties was subject to TP adjustments in its home country.

Prioritized applications

An APA application that meets one of eight criteria listed in the Announcement will be prioritized in proposal review and application acceptance. Among them include whether:

- the applicant has fully complied with the China inter-company transaction disclosure and contemporaneous documentation requirements, and the information disclosed is reasonably satisfactory;

- the applicant was subject to a TP audit, and the audit has been closed;

- the application materials (especially analysis on value chain and location-specific advantages) are complete and thorough, and the pricing and calculation methods are reasonable; and

- in the case of a bilateral APA application, the other tax authority has shown great interest and attached importance to the intended APA.

While these are not compulsory for filing APA applications, missing them in practice may result in more time spent and less attention received from the China tax authority.

Arm’s length principle

If an inter-quartile range has been used to establish the arm’s length price or profit level for an APA period, the applicant’s financial results during this period should be consistent with the median of the identified inter-quartile range, as provided in Article 12 of the Announcement. In particular, the tax authority:

- will be entitled to impose TP adjustments based on the median, if the applicant’s transfer prices or financial results fall out of the inter-quartile range; and

- may refuse to renew the APA, if the applicant’s average transfer price or financial results in the APA period fall below the median of the inter-quartile range.

Article 12 does not specifically address the circumstance where an applicant’s financial result sits in the lower quartile of the identified inter-quartile range. Presumably, the applicant may be permitted to conduct a voluntary adjustment at the end of an APA period, so that the average transfer price or financial result meets the median and the APA renewal can be accepted.

Extended rollback

The Announcement confirms that an APA agreed may roll back up to 10 years, instead of the five years generally expected under the previous Circular 2. This provides an opportunity for MNCs to resolve historical TP issues through an APA application, but it remains unclear how the rollback mechanism and historical general tax issues would be reconciled. For example, if there was a certain tax controversy in a previous year, whether that year can still be covered under the rollback; or if there were certain tax adjustments against a previous year, whether the rollback should be applied as after or before the tax adjustment. There could be more complicated issues in practice considering the recent substantial changes in China’s corporate tax system.

No prescribed time limit

The Announcement does not include a time frame for the APA application procedure—and there will be no deadlines for the tax authority’s review or acceptance of the application. This means it is the applicant’s responsibility to meet the prioritized criteria and provide all necessary the information and documents.

MNC considerations

In a nutshell, the SAT has very clearly signaled its determination to improve the efficiency and quality of China APA applications. The Announcement significantly changes the application procedure to allow for the tax authority to conduct a detailed review and assessment of a proposal before formally acceptance. At the same time, it imposes additional requirements on value and location-specific advantage analyses and overseas related party information disclosure, and pledges to prioritize applications supported by complete compliance records and in-depth analysis.

MNCs should expect a China APA application to be more difficult and challenging under these new rules. A proper assessment of an APA opportunity must include, among other factors, a consideration of the bandwidth of the SAT and local tax authority, the APA application’s attractiveness to the Chinese tax authorities, the opportunity for the APA application to be prioritized, the quality and strength of the underlying value chain and supply chain analysis, the availability and strength of the location-specific advantage analyses, and the practicality of achieving the median profit level of the proposed inter-quartile range. Once starting an APA application procedure, understanding and meeting the China tax authority’s expectations during the proposal and evaluation steps is crucial.

Daniel Chan, Partner, Windson Li, Of counsel, and Henry Ji, Associate DLA Piper, Hong Kong and Beijing